Three Companies Hold the Keys (And They Don't)

In The Uncomfortable Parts I said I was dependent on companies I can't influence. A single government memo this month proved the dependency goes deeper than I'd written: even the companies I depend on are themselves at the mercy of states and suppliers they can't influence either.

When I wrote The Uncomfortable Parts last month, I had a section called "I'm dependent on companies I can't influence." I described single-supplier risk, named the three companies that control the infrastructure, cited the lock-in numbers, and moved on. I thought I'd been honest and clear about it.

Then the directive came, and I realised I'd only described the top layer.

On 12 June 2026, at 5:21pm Eastern, Anthropic received a directive from the US government ordering it to disable Claude Fable 5 and Mythos 5 for every foreign national, inside the US or outside it, including its own foreign-national employees [1]. Anthropic complied by switching the models off entirely for everyone, since that was the only way to be sure it wasn't serving a foreign national by mistake [1]. The (supposedly) most capable model on the market had been live for a few days. Then it was gone, worldwide, in an afternoon, with no detail given beyond a national-security concern that the government believed someone had found a way to jailbreak it [2].

I'm a foreign national. I'm Canadian, building on Anthropic's API from a town in northern Alberta. I am exactly the person that directive was written about.

So the section I wrote last month was true but shallow. "I'm dependent on companies I can't influence" is the simple version. The truer version is this: the companies I depend on are themselves dependent on states and suppliers they can't influence, and this month I watched the whole chain whip at once. This is what I actually want to write about now.

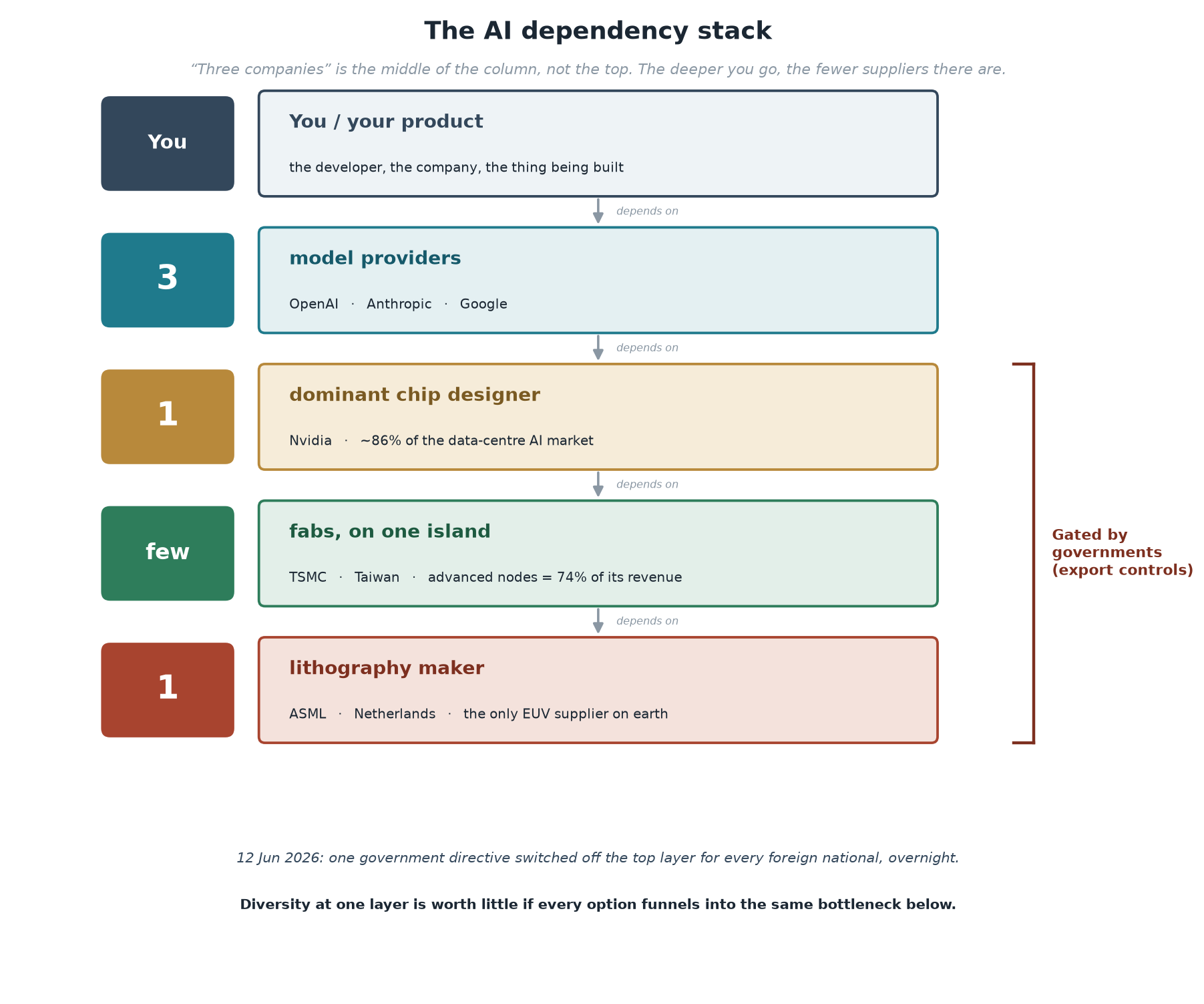

The keys aren't held by three companies

The easy framing, the one I used myself, is that AI infrastructure is concentrated in three companies. OpenAI, Anthropic, Google. Menlo Ventures puts Anthropic at 40% of enterprise LLM spend [3], 94% of IT leaders cite vendor lock-in as a material concern [4], and the natural conclusion is that these three firms hold the keys to a large and growing share of the software being built today.

That framing is correct as far as it goes. It just stops one layer too early, because it treats the three companies as the top of the stack. They aren't. They're the middle.

Concentration isn't a single chokepoint. It's a stack of them, and each layer is a point of control held by someone who can shut the layer below without asking the layer above. Once you see it as a stack, "three companies hold the keys" stops being the reassuring version (at least there's competition between three) and becomes the alarming one (every one of those three sits on top of the same narrowing column of dependencies, and the column ends in governments).

Let me go down the stack, because the specifics are the point.

Layer one: the model providers

This is the layer I already wrote about, so I'll be brief. Three companies control the frontier. I chose Anthropic deliberately, intially, with full awareness of the single-supplier risk, because I think their approach to safety is more serious than the alternatives. I said last month that choosing the dependency knowingly doesn't reduce the risk, it just means I can't pretend I didn't see it coming. So in the interest of taking my own medicine, I then adapted my full workflow to be more supplier-independent, by incorporating OpenAI's Codex into my development process. Job done, no?

What I didn't fully reckon with is that my provider's own control over the layer it sells is conditional. Anthropic can set its pricing, deprecate its models, and change its policies, and those are the risks I listed. But Anthropic cannot decide to keep serving Fable 5 to me if the US government says no. The provider I picked turns out to be a tenant, not an owner, of the very thing I'm renting from it. Happily I still had full access to the latest model from Codex (GPT 5.5), but it's not like that doesn't face exactly the same risk as Fable - if the US government decides that the model is too 'powerful' for general release, it'll be pulled.

Layer two: the state

This is the layer the directive exposed.

The Fable directive wasn't a pricing change or a deprecation, the failure modes I'd planned for. It was a government reaching past Anthropic and switching off a product for an entire class of users defined by nationality. Anthropic didn't choose to cut me off. It was told to, and it had no realistic option but to comply, because the alternative to "disable the model" is "be a US company defying a national-security export directive," which is not a real alternative.

What makes this layer so much worse than the commercial risks is the speed and the unaccountability. A pricing change comes with notice. A deprecation comes with a migration window; Anthropic gave the Claude 3.x family roughly two months [5]. The directive came with neither. It arrived at 5:21pm and the model was off the same evening [1]. There was no consultation, no appeal I could file as a customer, and no detailed reason I could even evaluate. The justification was a national-security concern the government chose not to specify [2].

I spent years in governance and audit. I know what it means for a control to be outside your span of influence. This is the purest example I've encountered: the most important input to my business can be revoked, without warning or explanation, by an entity I have no relationship with, on the basis of a nationality I can't change. No contract protects me, because the contract is between me and Anthropic, and the directive went over Anthropic's head.

And here's the part that should bother anyone building on this infrastructure regardless of where they sit: the precedent doesn't have a natural boundary. The directive was scoped to foreign nationals and the two most capable models. But the mechanism, a government deciding which models may be served to whom, is now demonstrated and operational. The scope of any future use of it is a policy choice, not a technical limit.

What the eleven days since have shown

I drafted most of the above the week it happened. I've sat on it since, partly to see whether the situation would resolve and partly because I wanted to write the structural argument rather than the hot take. It hasn't resolved. As I write this, eleven days on, both models are still dark for everyone [13]. An Anthropic executive said publicly that the company was "very confident" access would return "in the coming days" [14]. The coming days came and went. That, on its own, makes the point: the company at the centre of this couldn't tell its own customers when, or whether, the thing they depend on would come back, because the decision was never the company's to make.

There has been one apparent thaw, and it proves the point rather than softening it. On 19 June, after a G7 meeting with Anthropic's CEO, the US president told an interviewer that he no longer saw the company as a national-security threat: "not now, but a week ago, maybe" [19]. Asked whether he'd ease the restrictions, he said, "I would, but I'm not sure I have to" [19]. Read that back. The most capable models on the market were switched off for the entire world, and the mechanism that might switch them back on is one man's shifting estimate of a company's character after a lunch. As I write this the directive is still formally in force and the models are still off [19]. Whether they return is, right now, a matter of mood at the top of a government, which is precisely the kind of input no business should have at the base of its stack.

The rest of the fallout has, if anything, strengthened the case I'm making rather than weakened it.

The legal basis turns out to be contested. Former Commerce Department officials have argued the directive may not even be valid, on the grounds that serving a model over an API isn't obviously an "export" under the rules being invoked [15]. I find that more alarming, not less. The control was applied first and the question of whether it was lawful is being argued after the model was already switched off. When the mechanism runs ahead of the legality, "is this allowed?" stops being a brake.

A bipartisan group of US House members has since written to the administration demanding the legal justification and asking whether other AI firms should expect the same treatment [16]. That's the precedent question I raised above, asked out loud by legislators within a fortnight. Nobody yet knows the answer, which is itself the answer: the boundary is undefined.

And the response abroad has been exactly the one you'd expect from people who just watched a dependency get used as a lever. Canada's prime minister framed it as a warning about over-reliance on a handful of US providers and urged allies to diversify [17]. France's president called the ban "strictly nationalist," and the EU floated a "trusted partner" scheme for access to advanced models [17]. I'm a Canadian founder reading my own government say, in public, that the thing I build on is a strategic vulnerability. I wrote that down as a worry a few weeks ago. Now I'm watching prime ministers and presidents say it back to me as policy.

I'll note one thing carefully, because it's been everywhere and most of it is unverified. A US senator relayed a claim that the model in question had broken into nearly all of a classified government network in hours [18]. It may be the real reason behind the directive. It is also disputed, undocumented, and not corroborated by Anthropic, and experts have suggested it more likely describes an internal red-team exercise than an actual breach [18]. I'm including it only because you'll have seen it, and because the gap between "a senator said it" and "anyone can verify it" is its own small illustration of the problem: the most consequential input to a lot of businesses was switched off over a justification that, as of now, nobody outside the room can evaluate.

Layer three: the chips

Still, that's "only" the state layer. Let's go down another layer to see how the concentration gets worse, not better.

Every one of those three model providers trains and serves on the same hardware. Nvidia holds roughly 86% of the data-centre AI accelerator market as of late 2025, up from about 25% in 2021, and around 92% of the discrete GPU market [6]. The frontier-model layer looks like an oligopoly of three. The layer it runs on looks like a near-monopoly of one.

So the three companies don't even compete on their most fundamental input. They are all customers of the same supplier, which means a constraint on Nvidia, a supply shortage, an allocation decision, a future export rule on the chips themselves, propagates to all three of them simultaneously. The apparent diversity at the model layer is sitting on a single point of failure one layer down.

This is why "at least there are three of them" provides less comfort than it seems to. Diversity at one layer is worthless if every option funnels into the same bottleneck at the next.

That said, the bottleneck is already breeding its own alternative, but perhaps for the worst possible reason. When the US cut Huawei off from TSMC-made chips in 2020, it didn't end Huawei's AI hardware ambitions, it forced them inward. Huawei's Ascend 910C, manufactured domestically, crossed into profitability in early 2025 at a roughly 40% yield, and Huawei now accounts for over 75% of China's domestic AI chip production, scaling toward an estimated 600,000 Ascend units in 2026 [10]. It isn't competitive with Nvidia at the frontier yet, and it leans on state subsidies and a protected home market to be viable at all [10]. But the direction is the point: the chokepoint didn't deny the capability, it relocated it. Cut off the supply and you don't remove the demand, you fund a parallel supplier.

Layer four: the fabs

You thought we were done? Incorrect! And that's because Nvidia doesn't make its own chips. It designs them and has them manufactured, overwhelmingly by TSMC in Taiwan. TSMC's advanced nodes, 7nm and below, accounted for 74% of its wafer revenue in the third quarter of 2025, with 3nm alone making up around 23% [7]. The most advanced chips in the world, the ones the AI buildout depends on, are made in a handful of fabs concentrated on a single island that sits in the most contested geopolitical position on the planet.

There's a name for this. People call it Taiwan's "Silicon Shield," the theory that the world's dependence on TSMC is itself a deterrent against conflict [7]. I'd put it less reassuringly: every global compute stack, including the entire AI stack, every model from all three providers, ultimately rests on continued political stability in the Taiwan Strait. TSMC is expanding into the US and Japan [8], which helps at the margin, but the leading edge is still overwhelmingly Taiwanese, and "the leading edge" is exactly the part the frontier models need.

So my dependency, traced all the way down, includes a geopolitical situation I have precisely zero influence over and which a great many people more powerful than me also can't control.

Incidentally, the same pattern from the chip layer repeats here. The Huawei chips I just described are built on SMIC's 7nm process, achieved through DUV multi-patterning rather than the EUV machines China can't buy [10]. SMIC is the domestic fab that exists in its current advanced form precisely because the leading-edge alternative was placed out of reach. Restricting access to TSMC's frontier didn't freeze China's manufacturing, it gave China a reason to build a second one. The fab concentration on Taiwan is real and it's a genuine risk to me. But the export controls meant to preserve that concentration are, layer by layer, dismantling it.

Layer five: the one machine that makes it possible

And below the fab, where you'd think the rabbit hole finally bottoms out, there's one more rung. The one almost none of us knew was there.

TSMC can't make those chips without extreme ultraviolet lithography machines, and there is exactly one company on Earth that makes them: ASML, in the Netherlands. ASML is the sole supplier of EUV systems worldwide and holds around 90% of the broader advanced lithography market [9]. Not the largest supplier. The only one. The most advanced chips in the world can only be made on machines from a single company in a single country.

And that company is itself gated by a government. Since 2019 the Dutch government, under sustained US pressure, has restricted which ASML machines can be exported and to whom, revoking licences as policy shifts [9]. So the bottom of the stack isn't a company at all. It's a Dutch export-licensing decision, shaped by Washington, governing the one machine that makes the chips that the one chip company designs that the three model providers all depend on that I (and probably you) build my products on.

And at the very bottom layer, the one that looked most like an unbreakable monopoly, the same predictable reaction is underway. Locked out of ASML's machines, China is building its own. SMEE delivered a 28nm immersion DUV system for testing in early 2025 [11], and a state-coordinated EUV effort led by Huawei and SMEE, pulling together more than 3,000 researchers and a domestically developed light source, is targeting functional chip output by 2028 [12]. The realistic timeline is probably later than that, and an EUV prototype is a long way from ASML's volume and precision. But the existence of the programme is the point. The single most concentrated chokepoint in the entire stack, the one company on Earth that makes EUV machines, produced the strongest possible incentive for someone to build a second one, and that someone has the resources of a state behind them.

This is the part of the geopolitics that I think gets missed in the comfortable version of the concentration story. The chokepoints aren't stable. Every layer of this stack that a government has weaponised - chips, fabs, lithography - has triggered a state-funded effort to route around it. The controls are real and they bite now. But they are also, slowly and expensively, manufacturing the exact competitor they were designed to prevent. The keys are concentrated today. The act of using them as a weapon is what guarantees they won't stay that way.

That's the full chain. Five layers, and it gets narrower as you go down, not wider. Me, then three providers, then one dominant chip designer, then a handful of fabs on one island, then one lithography company gated by two governments. The keys aren't held by three companies. They're held by a column that ends in states, and the three companies are renting from it just like I am.

Why I'm telling you this instead of solving it

When I wrote the dependency section last month, I gestured at (and built some) mitigations: multi-provider abstraction, local models, open-weight fallbacks, contract protections. They're all worth doing, and I do some of them. But this clarified how far they actually reach, and the honest answer is: not as far as I'd like.

Multi-provider abstraction protects me from one provider's pricing or deprecation. It does nothing against a directive that hits a class of models across the industry, or against a constraint that propagates from the shared chip layer to all providers at once. Switching from Anthropic to a competitor is moving between tenants in the same building, on the same foundation, gated by the same governments.

Local and open-weight models are the one hedge that genuinely holds, and they're the one I take most seriously now, because a model running on hardware I control can't be switched off by a memo. The catch is that the open-weight models I can run locally are not the frontier, and the gap between them and the frontier is exactly the capability that made Fable worth restricting in the first place. The hedge works precisely to the extent that I'm willing to give up the capability that created the dependency. That's a real trade-off, not a free one, and I won't pretend otherwise.

And none of it touches the bottom three layers. There is no abstraction I can write, no contract I can sign, and no model I can self-host that insulates me from a chip allocation, a fab disruption, or a lithography export rule. Those are structural, and they require structural responses from people far above my pay grade. The most I can do at my layer is know the chain is there, keep the local fallback warm, and not build anything whose survival depends on the top of the stack staying switched on.

I keep coming back to a line I wrote last month. The structural problems require structural responses, and most of those responses haven't arrived yet. This was the moment that stopped being an abstract sentence for me. The (apparently) most capable model in the world disappeared from my workflow because of a decision made by people I'll never meet, transmitted through a company that had no choice, about a category I happen to fall into.

Three companies hold the keys. But they don't, really. They're holding them for someone else, and this month that someone else took them back, and whether they're handed over again is, as I write this, still up to him.

Sources

- Anthropic — Statement on the US government directive to suspend access to Fable 5 and Mythos 5 — Directive received 12 June 2026 at 5:21pm ET ordering suspension of access for all foreign nationals; Anthropic disabled both models for all customers to ensure compliance. Also TIME, Al Jazeera.

- Fortune — 'Fix this code.' The three little words behind the US government decision to shut down Fable and Mythos — Government's stated concern relates to a method of bypassing ("jailbreaking") Fable 5; no further detail disclosed. Also Fortune — Anthropic disables Fable and Mythos following export ban.

- Visual Capitalist — Ranked: AI Models U.S. Businesses Pay For — Menlo Ventures data on enterprise LLM spend shares (Anthropic 40%, OpenAI 27%, Google 21%).

- Amundson Strategic — What Your Board Doesn't Know About AI Vendor Lock-In — 94% of IT leaders cite vendor lock-in as a material concern.

- LemonData — AI API Market 2026 Trends — Claude 3.x retirement timeline (October 2025 to January 2026), roughly a two-month deprecation window.

- CarbonCredits — NVIDIA Controls 92% of the GPU Market in 2025 — Nvidia ~86% of the data-centre AI accelerator market in late 2025 (up from ~25% in 2021), ~92% of the discrete GPU market. Also Statista — Data center/AI chip revenue of Nvidia, AMD & Intel 2025.

- TSMC — FY2025 Q3 6-K — Advanced technologies (7nm and below) = 74% of wafer revenue in Q3 2025; 3nm = 23%. "Silicon Shield" framing via FinancialContent — A Deep Dive into the Silicon Shield.

- Focus Taiwan — TSMC expanding 3nm capacity in Taiwan, U.S., Japan — Leading-edge expansion beyond Taiwan, with the bulk of advanced capacity still domestic.

- SDxCentral — Dutch government revokes some ASML lithography export licenses, due to US pressure — ASML is the sole global supplier of EUV systems and holds ~90% of the advanced lithography market; Dutch export licences restricted since 2019 under US pressure. Also CNBC — ASML 2025 outlook shows US chip export curbs impacting China sales.

- TrendForce — China Advances in AI Chips: Huawei Boosts Yield to 40%, Making Ascend Line Profitable — Ascend 910C on SMIC 7nm (N+2) via DUV multi-patterning; ~40% yield, first profitability, reliance on subsidies and a protected market. Huawei >75% of China's domestic AI chip production and scaling toward ~600,000 Ascend units in 2026 via RCR Wireless — Huawei to double output of Ascend AI chips and Digitimes — Huawei Ascend 910C reportedly hits 40% yield. Both are a direct response to the 2020 US order halting TSMC production of Huawei chips.

- Digitimes — China accelerates DUV lithography breakthroughs with patents and testing — SMEE delivered a 28nm immersion DUV system (SSA800 series) for testing in early 2025, enabling multi-patterning below 28nm.

- Asia Times — Made-in-China EUV machine targets AI chip output by 2028 — State-coordinated EUV programme led by Huawei and SMEE, 3,000+ researchers, domestically developed LDP light source, targeting functional chips by 2028 (2030 seen as more realistic). Context via TrendForce — Decoding China's Lithography Push to Challenge ASML.

- TechJack Solutions — Claude Fable 5 / Mythos 5 suspended under US export controls (status tracker) — As of 22 June 2026, both models remain suspended per Anthropic's status page; no restoration announced. Corroborated by Anthropic's statement page, which carries no post-12-June restoration update.

- Korea JoongAng Daily — Anthropic confident of re-enabling Mythos, Fable 5 access "in coming days," executive says — Anthropic Managing Director of International Chris Ciauri, speaking in Seoul, said the company was "very confident" the models would return "in the coming days." No specific date given; access had not returned as of writing.

- Gizmodo — Feds' legal basis for ban on Anthropic's most powerful models looks increasingly shaky — Former Commerce Department policy adviser argues serving a model over an API may not constitute an "export" under the Export Administration Regulations, casting doubt on the directive's legal footing. Also Washington Post.

- Washington Post — House members want answers on export controls placed on Anthropic, Fable — A bipartisan group of US House members wrote to the administration (18 June 2026) demanding the legal justification for the directive and asking whether rival AI firms should expect similar treatment.

- Al Jazeera — US export ban on Anthropic's AI models further strains alliances — Canadian PM Mark Carney framed the ban as a warning about over-reliance on a few US AI providers and urged diversification; French President Macron called the ban "strictly nationalist"; the EU floated a "trusted partner" scheme for advanced-model access. Also Globe and Mail, Euronews.

- Security Affairs — Anthropic's Mythos AI reportedly broke into NSA classified systems in hours (claim) — Sen. Mark Warner relayed a claim, attributed to the NSA/Cyber Command chief, that Mythos breached nearly all of a classified network "in hours." Disputed and unverified: no published incident report, no NSA/CISA bulletin, no Anthropic corroboration; experts suggest it more likely describes an internal red-team exercise. Dispute coverage via The Cybersec Guru and Digg — Experts dispute Warner's claim.

- The Next Web — Trump says he no longer views Anthropic as a national security threat — In an Axios interview published 19 June 2026, President Trump said "not now, but a week ago, maybe" when asked if he saw Anthropic as a threat, crediting a 17 June G7 meeting with CEO Dario Amodei; on easing the restrictions he said "I would, but I'm not sure I have to." The Commerce Department directive remained formally in force and both models were still disabled. Independent confirmation via Cryptopolitan.